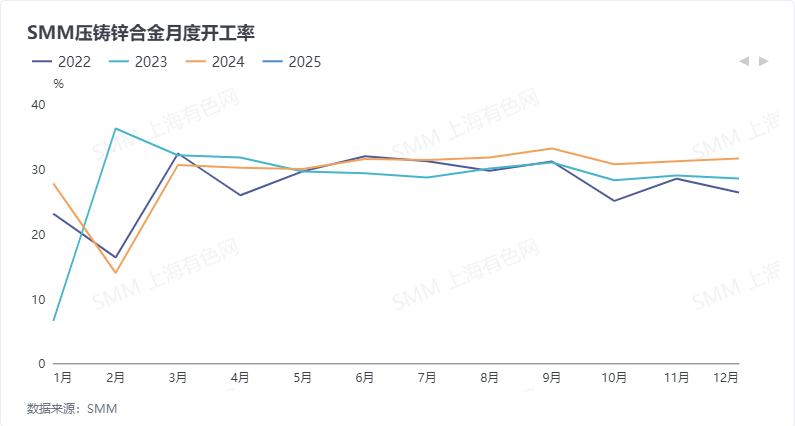

SMM February 13 News:

According to SMM data, as of the week of January 17, the weekly finished product inventories of die-casting zinc alloy enterprises reached 16,400 mt, hitting a two-year high. In the first week after the Chinese New Year holiday (February 7), the finished product inventories of enterprises remained at a high level of 15,725 mt. Meanwhile, from the perspective of total inventories (raw materials + finished products), the total inventory of die-casting zinc alloy enterprises before the 2025 Chinese New Year was 22,600 mt, a decrease of 2,880 mt compared to 25,480 mt in 2024, but an increase of 3,825 mt compared to 18,775 mt in 2023. Overall, this year's inventory changes were slightly lower than last year but slightly higher than the year before. What caused such high finished product inventories for enterprises this year?

First, from the perspective of zinc prices, before the 2023 Chinese New Year, zinc prices remained at a high level of 24,500 yuan/mt, increasing stocking costs for enterprises. At the same time, downstream demand was weak under high prices, leading enterprises to reduce stocking demand. Before the 2024 Chinese New Year, zinc prices continued to decline, and enterprises held a bearish outlook on subsequent zinc prices, resulting in relatively low finished product inventories. Before the 2025 Chinese New Year, although zinc prices showed a downward trend, enterprises adopted a cautious attitude toward subsequent zinc prices due to US tariff issues, leading to a significant increase in finished product inventories.

Secondly, from the perspective of weekly raw material inventories of enterprises, as of the week of January 17, the raw material inventories of die-casting zinc alloy enterprises were 7,385 mt. In the first week after the Chinese New Year holiday (February 7), raw material inventories remained at a low level of 7,050 mt. According to communication with enterprises, their stocking plans for the Chinese New Year largely followed the strategy of "leaving almost no raw materials and converting everything into finished products," which significantly increased finished product inventories. This situation was mainly due to enterprises' cautious outlook on post-holiday zinc prices and order trends.

So, how will the inventories of die-casting zinc alloy enterprises change in the future?

From the perspective of zinc prices, affected by US tariff news and the market's continued wait-and-see attitude toward the US Fed's interest rate cut, domestic and international zinc prices are expected to remain volatile. In such an environment, enterprises are expected to continue adopting cautious stocking strategies, mainly based on actual demand. Meanwhile, according to SMM, some large die-casting zinc alloy enterprises in Zhejiang and Guangdong are still on holiday, and few end-user downstream enterprises have resumed operations. As transportation gradually recovers, enterprises are expected to primarily consume finished product inventories in the near term, leading to a significant reduction in finished product inventories. Raw material inventories, however, are expected to increase slightly after the Lantern Festival as enterprises resume operations.